Macroeconomic performance

Between 2014 and 2016, real GDP growth was anemic and picked up to 8.5% in 2017, reaching about 6.2% in 2018, driven mainly by the oil sector. The budget account deficit improved marginally, from 5.9% in 2017 to 5.7% in 2018, as did the current account deficit, which fell from 4.5% in 2017 to 4.4% in 2018. Inflation fell back below 10%, to 9.8%, and average lending rates fell from 4.71% to 16.23% in September 2018. The Ghanaian cedi stabilized against major currencies, with the exception of a slight depreciation against the U.S. dollar in the second quarter of 2018.

In September 2018, Ghana recovered its GDP from 2006 to 2013. The reworked 2017 GDP is 24.6% higher than the previous 2017 GDP. Private consumption rose to 6.2% in 2018. Growth is expected to grow by 7.3% in 2019 and then by 5.4% in 2020 as the effects of increased oil production from new wells fade.

Outlook: positive and negative factors

Despite the positive outlook, Ghana faces potential difficulties. At the national level, the government has to meet gross financing requirements (20% of GDP) while national income represents around 10%. In addition, the external public debt ratio is high, from 40.5% of GDP in 2017 to 38.5% in 2018. Internationally, dependence on commodity exports continues to expose the economy to international commodity price shocks, and risks weakening GDP growth and the current account balance. Private domestic consumption is also expected to slow, to 4.9% of GDP in 2019 and 3.5% in 2020. Potentially low oil prices could reduce export earnings and thus revenues.

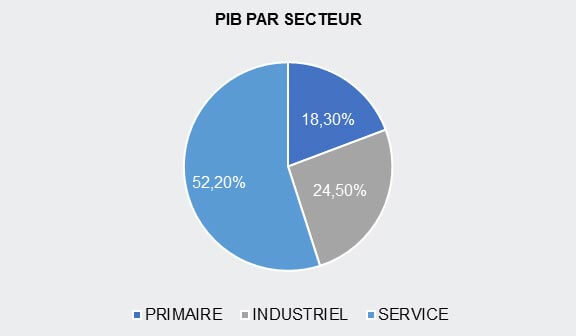

Continued strengthening of external demand for oil and cocoa will boost growth in the medium term. But years of growth based on extractive industries have failed to address growing inequalities or create decent jobs. Agriculture remains the main economic activity. Low agricultural productivity has triggered a vast movement of the workforce from this sector into essentially informal services in urban areas. While employment levels are high, they are of mediocre quality. Proactive measures to increase productivity are being launched through a process of industrialization, defined in the ten-point national industrialization program.

Ghana is gradually building up its industrial capacity, and growth in industry is expected to reach 9.8% in 2019 and 5.9% in 2020. Machinery imports are increasing rapidly: between 2000 and 2017, their total value quadrupled to 670 million USD. These imports have a substantial negative effect on the country's current account, but reflect a gradual shift towards industrialization. However, government capital spending has been on the decline since 2016. Private sector participation in industrialization is therefore more important, as envisaged in the state's economic transformation program.

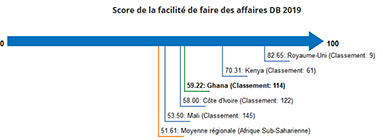

In a context of high indebtedness and low public and private savings, the State's main recourse for financing its economic transformation program is foreign direct investment. Such financing will require a focus on achieving sustainable results in terms of macroeconomic stability and the business environment. It will also be necessary to promote the rational mobilization of domestic revenues to accelerate the implementation of debt sustainability measures and increase fiscal space for public and social spending.

Source: African Economic Outlook (AEO) 2019